📊 Full opportunity report: The pyramid cracks. What agentic AI does to the consulting leverage model. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

Generative AI is breaking the classic consulting pyramid, reducing analysis-driven work and boosting deployment services. Firms are reorganizing, with some shrinking analyst roles while others expand implementation capacity. The industry is splitting into distinct segments, with long-term talent pipelines at risk.

Generative AI is significantly disrupting the traditional consulting leverage pyramid, leading to firm-specific restructuring and a reallocation of value from analysis to deployment services. This development impacts the industry’s core economic model and talent pipeline, with some firms reducing headcount in analysis roles while others expand into AI deployment.

Recent industry data and firm reports show that AI is commoditizing the analysis work that historically formed the base of the consulting pyramid. McKinsey, for example, has reduced non-client-facing roles by approximately 10%, citing automation of research and synthesis tasks. Meanwhile, Accenture has posted record bookings and increased its AI and data workforce, emphasizing deployment and scaling services as new revenue streams.

The core argument is that AI is causing a structural split: firms focused on analysis face margin compression and talent pipeline issues, while those specializing in large-scale implementation and AI deployment are experiencing growth. This split results in a reorganization rather than an industry contraction, with the traditional leverage model under threat.

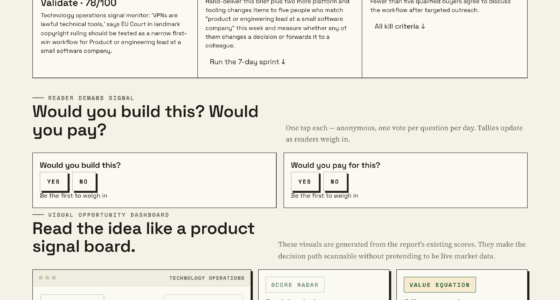

The pyramid cracks.

What agentic AI does

to the consulting

leverage model.

per McKinsey’s own Quantum Black

non-client-facing cuts coming

85,000+ AI & data professionals

growth % — the compression, visible

before AI

for the same output

The compression is a reallocation, not a contraction. The demand for help migrates from analysis — which AI commoditizes — to deployment — which AI creates demand for. The pyramid that monetized analysis-by-juniors compresses. The firm that monetizes deployment-at-scale grows.Thorsten Meyer · The Pyramid Cracks · Enterprise Reorg 02

Implications of AI-Induced Industry Restructuring

This shift fundamentally alters the consulting industry’s economic model, threatening the long-term talent pipeline and changing the nature of client engagement. Firms that adapt to focus on deployment and implementation are positioned for growth, while those reliant on analysis face margin squeeze and talent attrition. The industry’s core leverage structure is fragmenting, with potential long-term consequences for firm sustainability and talent development.

Perplexity AI From Beginner to Pro: The Complete 2026 Guide to Using AI Search to Get Accurate Answers, Verify Sources, and Stay Ahead (The AI Tools for Beginners Series: 2026 Edition)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Industry Background and AI’s Impact on Consulting Economics

The traditional consulting leverage pyramid relies on a large base of junior analysts performing document-heavy, repetitive work, billed at high margins. Recent advancements in generative AI have commoditized much of this work, leading to layoffs and headcount reductions at firms like McKinsey and KPMG. Conversely, firms like Accenture are expanding their AI deployment services, capitalizing on new opportunities created by AI’s capabilities.

The industry has been gradually shifting toward value-based and implementation services, but AI accelerates this trend, creating a clear divide between firms focused on analysis versus those focused on execution. The structural change is ongoing, with some firms already adjusting their talent and service offerings accordingly.

“The leverage pyramid that defined elite consulting is the most exposed structure in professional services because its economics depend on billing out a large base of juniors doing exactly the work AI now does.”

— Thorsten Meyer

![Express Schedule Free Employee Scheduling Software [PC/Mac Download]](https://m.media-amazon.com/images/I/41yvuCFIVfS._SL500_.jpg)

Express Schedule Free Employee Scheduling Software [PC/Mac Download]

- User-friendly drag & drop interface: Simple shift planning

- Manage time-off and leave: Add sick leave, breaks, holidays

- Email schedules to staff: Direct email schedule distribution

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unclear Long-Term Industry and Talent Pipeline Effects

It remains uncertain how deeply the talent pipeline will be affected over the next decade, especially whether firms will successfully pivot toward deployment or face long-term shortages of senior talent. The precise pace and scope of industry fragmentation are still developing, and some firms may adapt more quickly than others.

The No-BS Guide to AI for Trading & Market Research: How to Use ChatGPT, Claude & AI Tools for Market Analysis, Stock Research & Data-Driven Trading … … Required (The No-BS AI Playbooks Book 3)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Expected Industry Reorganization and Talent Shifts

Industry observers expect continued restructuring, with firms increasingly specializing either in deployment or analysis. Long-term, firms that fail to pivot away from analysis-heavy models may face sustained margin pressures and talent shortages. Monitoring firm-by-firm adaptations and talent pipeline health will be critical over the coming 12-24 months.

Ultimate CI/CD for Platform Engineering: Master DevOps Pipelines, GitOps, DevSecOps, Infrastructure as Code, Multi-Cloud Deployment, and AI-Driven Delivery Automation (English Edition)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

How is AI changing the consulting industry’s business model?

AI is commoditizing analysis work, reducing the need for large junior analyst teams, and shifting the industry toward deployment and implementation services that AI cannot perform autonomously.

Are consulting firms shrinking overall because of AI?

Not necessarily. The industry is reorganizing, with some firms reducing analysis roles while others expand deployment and AI scaling services. The overall size may stay stable or grow, but the internal structure is changing.

What are the long-term risks for firms heavily reliant on analysis work?

They face margin compression, talent pipeline issues, and potential obsolescence if they cannot pivot toward execution and deployment services that AI cannot replace.

Will the consulting industry overall shrink due to AI?

Industry experts suggest it will split rather than shrink, with some segments growing and others contracting. The value shifts toward firms capable of large-scale implementation.

What does this mean for consulting talent pipelines?

The traditional path from analyst to partner may be disrupted, risking fewer senior leaders in the future if firms cut back on training and hiring analysts now.

Source: ThorstenMeyerAI.com